Our new paper on CPI and core CPI is now available via MPRA.

Abstract

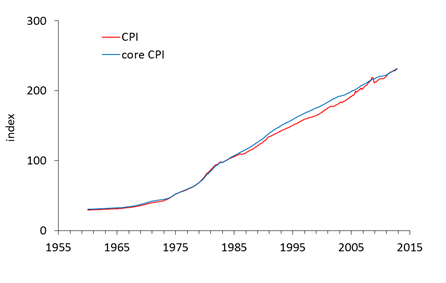

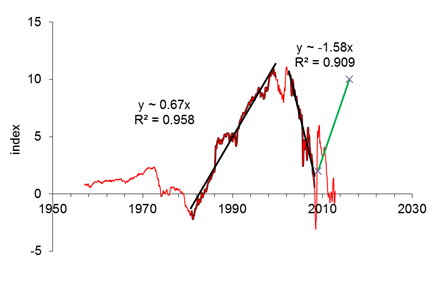

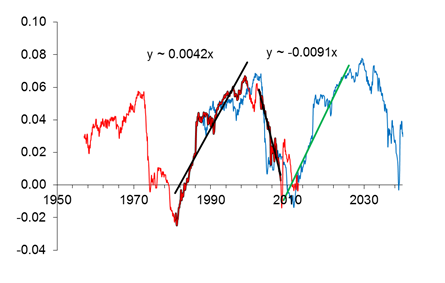

Five years ago, we found three distinct periods characterized by sustainable quasi-linear trends in the difference between the headline consumer price index (CPI) and the core CPI in the USA. Then we revealed similar behavior in the differences between the CPI and indices of various consumer expenditure categories. We estimated the duration of these trends which varies in a wide range from 8 years to more than 20 years. The transition periods to new trends span shorter intervals of 2 to 5 years. The transition is characterized by a higher level of volatility in the studied CPI differences. In this study, we revisit the revealed trends and transition periods using additional CPI estimates between 2008 and 2012. It is found that our major predictions are right: the headline CPI intersected the core CPI in 2011 and both variables have been evolving in sync since then. The difference between the core CPI and the index of energy has been suffering a transition period since 2008 with extremely high fluctuations. The index of food has been growing relative to the core CPI and did not reach its turning point. The difference between the core CPI and the index of housing passed through its transition period in 2008. When normalized to the CPI, the differences associated with energy and housing demonstrates clear periodicity. The observed trends and periodicity allow predicting the evolution of energy, food, and housing at a horizon of twenty five and more years. The consumer price index of energy may fall in 2013 by ten to twenty per cent from the 2012 level. The periodicity of the related normalized difference implies that this fall may extend into the second half of the 2020s. The housing index will be also falling relative to the core CPI, partly due to its energy related components. It is not excluded that the food price index will be rising another five to ten years. The secular fall in energy and housing prices may induce a lengthy period of very low inflation.

Abstract

Five years ago, we found three distinct periods characterized by sustainable quasi-linear trends in the difference between the headline consumer price index (CPI) and the core CPI in the USA. Then we revealed similar behavior in the differences between the CPI and indices of various consumer expenditure categories. We estimated the duration of these trends which varies in a wide range from 8 years to more than 20 years. The transition periods to new trends span shorter intervals of 2 to 5 years. The transition is characterized by a higher level of volatility in the studied CPI differences. In this study, we revisit the revealed trends and transition periods using additional CPI estimates between 2008 and 2012. It is found that our major predictions are right: the headline CPI intersected the core CPI in 2011 and both variables have been evolving in sync since then. The difference between the core CPI and the index of energy has been suffering a transition period since 2008 with extremely high fluctuations. The index of food has been growing relative to the core CPI and did not reach its turning point. The difference between the core CPI and the index of housing passed through its transition period in 2008. When normalized to the CPI, the differences associated with energy and housing demonstrates clear periodicity. The observed trends and periodicity allow predicting the evolution of energy, food, and housing at a horizon of twenty five and more years. The consumer price index of energy may fall in 2013 by ten to twenty per cent from the 2012 level. The periodicity of the related normalized difference implies that this fall may extend into the second half of the 2020s. The housing index will be also falling relative to the core CPI, partly due to its energy related components. It is not excluded that the food price index will be rising another five to ten years. The secular fall in energy and housing prices may induce a lengthy period of very low inflation.